What Is a Tracking Error?

Tracking error is the divergence between the price behavior of a position or a portfolio and the price behavior of a benchmark. This is often in the context of a hedge fund, mutual fund, or exchange-traded fund (ETF) that did not work as effectively as intended, creating an unexpected profit or loss.

Tracking error is reported as a standard deviation percentage difference, which reports the difference between the return an investor receives and that of the benchmark they were attempting to imitate.

Key Takeaways

- Tracking error is the difference in actual performance between a position (usually an entire portfolio) and its corresponding benchmark.

- The tracking error can be viewed as an indicator of how actively a fund is managed and its corresponding risk level.

- Evaluating a past tracking error of a portfolio manager may provide insight into the level of benchmark risk control the manager may demonstrate in the future.

Tracking Error

Understanding a Tracking Error

Since portfolio risk is often measured against a benchmark, tracking error is a commonly used metric to gauge how well an investment is performing. Tracking error shows an investment’s consistency versus a benchmark over a given period of time. Even portfolios that are perfectly indexed against a benchmark behave differently than the benchmark, even though this difference on a day-to-day, quarter-to-quarter, or year-to-year basis may be ever so slight. The measure of tracking error is used to quantify this difference.

Tracking error is the standard deviation of the difference between the returns of an investment and its benchmark. Given a sequence of returns for an investment or portfolio and its benchmark, tracking error is calculated as follows:

Tracking Error = Standard Deviation of (P — B)

- Where P is portfolio return and B is benchmark return.

From an investor’s point of view, tracking error can be used to evaluate portfolio managers. If a manager is realizing low average returns and has a large tracking error, it is a sign that there is something significantly wrong with that investment and that the investor should most likely find a replacement.

It may also be used to forecast performance, particularly for quantitative portfolio managers who construct risk models that include the likely factors that influence price changes. The managers then construct a portfolio that uses the type of constituents of a benchmark (such as style, leverage, momentum, or market cap) to create a portfolio that will have a tracking error that closely adheres to the benchmark.

Special Considerations

Factors That Can Affect a Tracking Error

The net asset value (NAV) of an index fund is naturally inclined toward being lower than its benchmark because funds have fees, whereas an index does not. A high expense ratio for a fund can have a significantly negative impact on the fund’s performance. However, it is possible for fund managers to overcome the negative impact of fund fees and outperform the underlying index by doing an above-average job of portfolio rebalancing, managing dividends or interest payments, or securities lending.

Beyond fund fees, a number of other factors can affect a fund’s tracking error. One important factor is the extent to which a fund’s holdings match the holdings of the underlying index or benchmark. Many funds are made up of just the fund manager’s idea of a representative sample of the securities that make up the actual index. There are frequently also differences in weighting between a fund’s assets and the assets of the index.

Illiquid or thinly-traded securities can also increase the chance of a tracking error, since this often leads to prices differing significantly from market price when the fund buys or sells such securities as a result of larger bid-ask spreads. Finally, the level of volatility for an index can also affect the tracking error.

Sector, international, and dividend ETFs tend to have higher absolute tracking errors; broad-based equity and bond ETFs tend to have lower ones. Management expense ratios (MER) are the most prominent cause of tracking error and there tends to be a direct correlation between the size of the MER and tracking error. But other factors can intercede and be more significant at times.

Premiums and Discounts to Net Asset Value

Premiums or discounts to NAV may occur when investors bid the market price of an ETF above or below the NAV of its basket of securities. Such divergences are usually rare. In the case of a premium, the authorized participant typically arbitrages it away by purchasing securities in the ETF basket, exchanging them for ETF units, and selling the units on the stock market to earn a profit (until the premium is gone). Premiums and discounts as high as 5% have been known to occur, particularly for thinly traded ETFs.

Optimization

When there are thinly traded stocks in the benchmark index, the ETF provider can’t buy them without pushing their prices up substantially, so it uses a sample containing the more liquid stocks to proxy the index. This is called portfolio optimization.

Diversification Constraints

ETFs are registered with regulators as mutual funds and need to abide by the applicable regulations. Of note are two diversification requirements: 75% of its assets must be invested in cash, government securities, and securities of other investment companies, and no more than 5% of the total assets can be invested in any one security. This can create problems for ETFs tracking the performance of a sector where there are a lot of dominant companies.

Cash Drag

Indexes don’t have cash holdings, but ETFs do. Cash can accumulate at intervals due to dividend payments, overnight balances, and trading activity. The lag between receiving and reinvesting the cash can lead to a decline in performance known as drag. Dividend funds with high payout yields are most susceptible.

Index Changes

ETFs track indexes and when the indexes are updated, the ETFs have to follow suit. Updating the ETF portfolio incurs transaction costs. And it may not always be possible to do it the same way as the index. For example, a stock added to the ETF may be at a different price than what the index maker selected.

Capital-Gains Distributions

ETFs are more tax-efficient than mutual funds but have nevertheless been known to distribute capital gains that are taxable in the hands of unitholders. Although it may not be immediately apparent, these distributions create a different performance than the index on an after-tax basis. Indexes with a high level of turnover in companies (e.g., mergers, acquisitions, and spin-offs) are one source of capital-gains distributions. The higher the turnover rate, the higher the likelihood the ETF will be compelled to sell securities at a profit.

Securities Lending

Some ETF companies may offset tracking errors through security lending, which is the practice of lending out holdings in the ETF portfolio to hedge funds for short selling. The lending fees collected from this practice can be used to lower tracking error if so desired.

Currency Hedging

International ETFs with currency hedging may not follow a benchmark index due to the costs of currency hedging, which are not always embodied in the MER. Factors affecting hedging costs include market volatility and interest-rate differentials, which impact the pricing and performance of forward contracts.

Futures Roll

Commodity ETFs, in many cases, track the price of a commodity through the futures markets, buying the contract closest to expiry. As the weeks pass and the contract nears expiration, the ETF provider will sell it (to avoid taking delivery) and buy the next month’s contract. This operation, known as the «roll,» is repeated every month. If contracts further from expiration have higher prices (contango), the roll into the next month will be at a higher price, which incurs a loss. Thus, even if the spot price of the commodity stays the same or rises slightly, the ETF could still show a decline. Vice versa, if futures further away from expiration have lower prices (backwardation), the ETF will have an upward bias.

Maintaining Constant Leverage

Leveraged and inverse ETFs use swaps, forwards, and futures to replicate on a daily basis two or three times the direct or inverse return of a benchmark index. This requires rebalancing the basket of derivatives daily to ensure they deliver the specified multiple of the index’s change each day.

Example of a Tracking Error

For example, assume that there is a large-cap mutual fund benchmarked to the S&P 500 index. Next, assume that the mutual fund and the index realized the following returns over a given five-year period:

- Mutual Fund: 11%, 3%, 12%, 14% and 8%.

- S&P 500 index: 12%, 5%, 13%, 9% and 7%.

Given this data, the series of differences is then (11% — 12%), (3% — 5%), (12% — 13%), (14% — 9%) and (8% — 7%). These differences equal -1%, -2%, -1%, 5%, and 1%. The standard deviation of this series of differences, the tracking error, is 2.50%.

Jose Luis Pelaez Inc / Getty Images

Definition

Tracking error is the variation between the performance of a portfolio and the performance of the portfolio’s benchmark over time.

Key Takeaways

- Tracking error is the variance between a portfolio’s returns and an index’s returns.

- Index funds have low tracking error and actively managed funds have high tracking error.

- Tracking difference is the return difference over a specific time period between a portfolio and index while tracking error shows how often the portfolio has different returns.

Definition and Examples of Tracking Error

Tracking error is the standard deviation difference of a sequence of portfolio returns and the returns of the benchmark the portfolio is based on or related to. For index funds, tracking error can be due to trading costs or other friction. For active funds, you should expect tracking error—the manager’s goal is to depart from the index and reduce correlation.

For actively managed funds or portfolios, tracking error is also called “active manager risk.” Risk and error generally have negative connotations, but, in this context, they are not necessarily negative.

Note

If you’re looking for an investment that will reduce correlation to a benchmark index, tracking error from that index is the goal. And for active managers to outperform the index, they necessarily must increase “risk.”

How Tracking Error Works

Let’s use two ETFs to show how tracking error works. The index fund we’ll use is the SPDR S&P 500 ETF (SPY). The actively managed fund we’ll use is the ARK Innovation ETF (ARKK).

SPY is an S&P 500 index fund. It exists to mimic the S&P 500 and is a passively managed fund. Any tracking error it has is friction to your investments over time. In its prospectus, the fund manager notes that fees and expenses can create an imperfect correlation between how the fund performs and its benchmark.

According to Fidelity, SPY’s tracking error in August 2021 is just 0.03. The asset class median is 10.41, which means the standard deviation of the difference in SPY’s returns and the actual S&P 500’s is low compared to other ETFs with the same stocks.

ARKK is an actively managed fund. According to its prospectus, ARKK seeks to invest in companies that it determines are engaged in disruptive innovation. It stands to reason that these types of companies would not have the same returns trends as an index made up of more stable stock.

As such, ARKK’s tracking error was 34.71 in August 2021, more than three times the median number. Again, this makes sense. If you were paying up (and ARKK’s expense ratio of 0.75% is far more than SPY’s of 0.09%) for an actively managed fund, you don’t want to end up with the same tracking error as a passively managed fund like SPY.

Tracking Error vs. Tracking Difference

Tracking error and tracking difference can both be used to analyze funds. While tracking error shows how often and how much the portfolio varies from the index, tracking difference is just the difference in return over a certain time period.

It is possible for a fund to have a high tracking error but low tracking difference if its returns are often different from the index but end up around the same at the end of the period.

Note

When analyzing a fund, you can use tracking error to find how consistently the fund tracks the index and tracking difference to find how close the performance is.

What It Means for Individual Investors

You can use tracking error to analyze a new fund or to ensure an existing investment is doing what it should be. If you’re looking for an index fund to diversify your portfolio, make sure it has low tracking error so that your returns aren’t being eaten away by costs. If you pay more for an actively managed fund to try to beat the market, you don’t want low tracking error because you could just buy an index fund and get the same result, in theory.

The Balance uses only high-quality sources, including peer-reviewed studies, to support the facts within our articles. Read our editorial process to learn more about how we fact-check and keep our content accurate, reliable, and trustworthy.

-

Fidelity. «SPY: Key Statistics.» Accessed Aug. 23, 2021.

-

Fidelity. «ARKK: Key Statistics.» Accessed Aug. 23, 2021.

Typically, tracking error explains the difference between the price behaviour of an index or benchmark and the position of an investment portfolio. To benefit from the same in terms of investment portfolio management, individuals need to become familiar with the concept and functioning of tracking error.

What is a Tracking Error?

Tracking error can be described as the relative risk of an investment portfolio when compared to its benchmark. It helps to measure the performance of a particular investment. It also aids to compare the performance of said investment against a concerned benchmark over a specific period. As a result, it serves as an indicator that helps to understand how well a fund is managed and what risks accompany it.

In simpler words, tracking error can be defined as the difference between an investment portfolio’s returns and the index it mimics or tries to beat. Often tracking error comes handy in gauging the performance of portfolio managers and is known as active risk and is mostly used for hedge funds, ETFs or mutual funds.

How to Calculate a Tracking Error?

Typically, there are two distinct ways of computing tracking error.

In the first method,

The cumulative returns of the benchmark are deducted from the investment portfolio’s returns –

Tracking Error = Return(P) – Return(i)

Here,

P = portfolio

i = index or benchmark

In the second method,

The portfolio returns are deducted from the benchmark first. Subsequently, the standard deviation of the outcome is calculated using this tracking error formula –

Tracking Error = Standard Deviation of (P – B)

Here,

P = Portfolio returns

B = Benchmark returns

Example of Tracking Error Calculation

Suppose, a large-cap mutual fund is benchmarked to S&P 500 index; its index and mutual fund realised the following returns over 5 years –

For S&P 500 Index –

12%, 5%, 13%, 9% and 7%

For Mutual Fund –

11%, 3%, 12%, 14% and 8%

From the available data, the series of difference stood at –

(11% – 12%) = -1%

(3% – 5%) = -2%

(12% – 13%) = -1%

(14% – 9%) = 5%

(8% – 7%) = 1%

With the help of the tracking error formula–

TE = Standard Deviation of (P – B)

= 2.79%

Any fund which shows a low tracking error signifies that its portfolio is following its benchmark quite closely. Contrarily, a high tracking error signifies that a fund is not following the set benchmark.

Notably, in index funds, the tracking error is never zero because of – expenses ratio, funds’ cash flow, and portfolio realignment due to changes in index composition.

What is a Good Tracking Error?

The type of investment portfolio decides whether a tracking error is good or bad. Typically, a smaller number indicates tightly bound portfolio earnings against benchmark returns. For instance, index fund managers opt for passive management and try to keep the differential returns significantly low to keep the tracking error low. Regardless, the decision of whether a certain degree of tracking error is good or bad depends entirely on the objectives of investment.

Factors Influencing Tracking Error

Several factors tend to influence the tracking error. For example, the table below highlights the factors that affect the ETF’s tracking error.

| Factor | Impact |

| Discounts & Premium to NAV | Bidding the market price of ETFs above or below their NAV results in discounts or premiums, which further leads to divergence. |

| Cash drag | Cash holdings are a factor with ETF as there is a significant time lag between receiving and reinvesting cash. This leads to variance in tracking error. |

| Optimisation | ETF providers cannot purchase thinly traded stock on benchmark without raising their prices upwards. This is why; they use samples that comprise more liquid stocks that can serve as a proxy to index. |

| Currency hedging | Owing to the cost of currency hedging, foreign ETFs with implementing the same usually do not follow any benchmark index. Factors like interest rates and volatility affect the price of hedging and in turn, influence the tracking error. |

| Capital gain distribution | Though ETFs are tax-efficient, they distribute taxable capital gains. Such distributions tend to impact performance differently than the index. |

| Changes in index | ETFs must keep up with the changes in the index. Generally, during the update, an ETF portfolio is likely to incur a transactional cost. |

| Security lending | ETF companies may counterbalance tracking errors with the help of securities lending. It is essentially a practice of lending holdings in ETF-based portfolios so that one could hedge funds for short selling. |

| Expense ratio | A high expense ratio influences the performance of ETF funds negatively. |

| Illiquidity and volatility | Illiquid securities often accompany a bid-ask spread which leads to errors in tracking. Similarly, the volatility of the benchmark also influences the tracking error. |

Significance of Tracking Error

These pointers indicate the importance of tracking error –

- Tracking error helps to measure and compare the performance of a portfolio with its concerned benchmark or index.

- Enables to gauge the consistency of excessive returns.

- It helps to convert the difference between an investment portfolio and concerned benchmark into a one-digit number for better comparison and understanding.

- It helps portfolio managers to ascertain how close a portfolio is to the benchmark.

- Tracking error serves as a neutral point and allows portfolio managers to make an informed decision.

- It helps investors to ascertain the significance of differences between the returns of benchmark and portfolio.

- Further helps to determine how active and proficient a portfolio manager’s investment strategy is.

Though there are numerous benefits of tracking error, it has its shares of limitations too.

Limitations of Tracking Error

Tracking error is extensively used to measure and compare both underperformance and outperformance of a fund against its benchmark. Typically, investors prefer a high tracking error in the event that there is a certain degree of outperformance. Alternatively, a low tracking error is preferred during consistent underperformance. Regardless, tracking error does not help distinguish between the two right away.

If you are planning to invest in passive funds, and index funds in general, you should be well aware of the concerned fund’s tracking error. In fact, tracking error of a mutual fund is as important as the fund’s historical performance. Read on to know what is tracking error is and the impact it could have on the returns of your mutual fund investment.

What is Tracking Error and What are its Consequences?

Tracking error is a measurement of a mutual fund’s financial performance against its benchmark over a period of time. It is calculated as the annualised standard deviation of the tracking difference in a certain period. In other words, you can check a fund’s tracking error to see how closely its portfolio follows the benchmark.

Fund managers of active funds can show a large tracking record as they try to get excess returns through active positioning. In contrast, passively managed funds aim to keep the tracking error as low as possible.

An index fund with a low tracking error shows that it is closely following the benchmark. It can indicate which funds are being more actively managed and their risk levels.

You should avoid index funds with a large tracking error as it indicates that there is something significantly wrong with the investment. This could indicate that a fund is taking unnecessary levels of risk like holding large amounts of cash or maintaining lopsided weightage. Always remember that most of the best index funds come with a low tracking error.

Formula To Calculate Tracking Error

Tracking error could be calculated through two methods. In the first method, the cumulative returns of the index is deducted from the portfolio’s returns. The tracking error formula would be:

Tracking Error = P – I, where P stands for portfolio returns and I stands for index or benchmark.

The second method would be to deduct portfolio returns from the benchmark or index and then the standard deviation of the outcome would be calculated with the following formula:

Tracking Error = P – B, where P stands for portfolio returns and B stands for benchmark returns. Let’s understand this with an example.

Tracking Error Example

For example, if the underlying index has delivered a return of 5% over one year, whereas the index fund has given a return of 4.9% over the same period, the tracking error of the index fund would be 0.1%.

So, as an investor, should you be concerned about tracking errors? Yes, of course!

Continuing with the above example, a tracking error of 0.1% indicates that you would be earning 0.1% less than what you would make if you had directly invested in the underlying index.

However, if the index fund replicates the underlying benchmark, why should there be a tracking difference?

What are the Reasons for Tracking Error?

The probable reasons for tracking error could be as follows:

1. Cash component

An index fund will not be able to invest 100% of the corpus in the index constituents. It has to maintain certain cash to meet redemption requests, day-to-day fund management charges, transaction costs, etc.

2. Corporate actions

Corporate actions such as dividends, bonuses, mergers, rights, preferential issues, etc., require the fund to re-align with the index’s composition. The scheme would require buying and selling portfolio components that add up to the transaction cost, affecting the returns of the fund.

3. Change in portfolio constituents

Sometimes, the underlying index may have new entrants or exits. To maintain the same composition as the underlying index, the index fund must purchase or sell those securities. However, there could be a mismatch in the price, circuit filters, etc., that may create a mismatch in quantities and eventually the returns.

Also read: Key Differences Between Direct Mutual Funds And Regular Mutual Funds

List of Index Funds with the Lowest Tracking Error

The following are the best index funds according to their tracking error:

| Name of the Index Fund | Tracking Error |

| Navi Nifty 50 Index Fund | 0.04% |

| HDFC Index Fund- Sensex Plan | 0.06% |

| SBI Nifty Index Fund | 0.10% |

| HDFC Index Fund- Nifty 50 Plan | 0.10% |

| UTI Nifty Index Fund | 0.11% |

| Nippon India Index Fund- Sensex Plan | 0.12% |

| DSP Nifty 50 Index Fund | 0.13% |

| ICICI Prudential Nifty Next 50 Index Fund | 0.13% |

*Note that the table is for educational purposes only.

Disclaimer: Mutual Fund investments are subject to market risks. Read all scheme related documents carefully before investing.

Does Tracking Error have Implications in Index Funds?

Tracking error helps measure the performance of a portfolio against its underlying index. An index fund with a low tracking error has a minimum deviation in terms of returns from the benchmark index.

You must check the tracking error of index funds rather than fund returns. It helps to pick an index fund with a lower tracking error to minimise the deviation in return from the benchmark index. Tracking error also helps you measure the consistency of excessive returns.

Also Read

Final Word

If passive funds are your go-to investment avenue, try to invest in funds with low tracking error. It also aids to gauge the performance of a particular fund against its concerned benchmark over a particular period of time.

In case you are looking to invest in funds that could give you market-level returns, try Navi Mutual Fund. With Navi’s mutual funds, you could explore a wide range of low-cost index funds, including the Navi Nifty 50 – a fund that comes with a significantly low tracking error.

FAQs

Q1. What is a good tracking error?

Ans: A smaller number usually indicates better portfolio earnings against the index benchmark. However, determining whether a tracking error is good or bad entirely depends on the objective of the investment.

Q2. When do active fund managers prefer high tracking error?

Ans: Often, active portfolio managers show high tracking error because they try to achieve excess return against the benchmark. On the contrary, passive fund managers seek low tracking error with return deviations coming from trading and liquidity costs, imprecise cash flows, tax costs, etc.

Q3. Why is tracking error important?

Ans: Tracking error helps portfolio managers understand how close they are to the benchmark.

Want to put your savings into action and kick-start your investment journey 💸 But don’t have time to do research? Invest now with Navi Nifty 50 Index Fund, sit back, and earn from the top 50 companies.

Disclaimer: Mutual Fund investments are subject to market risks, read all scheme-related documents carefully.

This article has been prepared on the basis of internal data, publicly available information and other sources believed to be reliable. The information contained in this article is for general purposes only and not a complete disclosure of every material fact. It should not be construed as investment advice to any party. The article does not warrant the completeness or accuracy of the information and disclaims all liabilities, losses and damages arising out of the use of this information. Readers shall be fully liable/responsible for any decision taken on the basis of this article.

Fixed Deposits vs Mutual Funds

9 February 2023

8 Kitchen Interior Design Ideas to Suit Every Style in 2023

8 February 2023

10 Best Nifty 50 Index Funds to Invest in 2023

7 February 2023

8 Best Health Insurance Plans in India in 2023

10 Best Personal Loan Apps in India in 2023

8 Living Room Interior Design Ideas to Suit Every Style in 2023

2 February 2023

Union Budget 2023 – 8 Key Highlights You Should Know

1 February 2023

Adani Stocks Have Crashed – Here’s Everything You Should Know

31 January 2023

10 Best Hybrid Funds to Invest in 2023

30 January 2023

Inside Anant & Radhika’s Lavish Engagement

27 January 2023

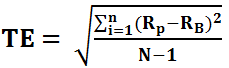

Formula for Tracking Error (Definition)

Tracking Error Formula is used in order to measure the divergence arising between the price behavior of portfolio and price behavior of the respective benchmark and according to the formula Tracking Error calculation is done by calculating the standard deviation of the difference in return of the portfolio and the benchmark over the period of time.

Tracking error is simply a measure to gauge how much the return of a portfolio or a mutual fund deviates from the return of an index it is trying to replicate in terms of the components of an index and also in the term of the return of that index. There are several mutual funds where the fund managers of that fund aim to construct the fund by closely replicating the stocks of a particular index, by trying to add stocks in his fund with the same proportion. There are two formulas to calculate the tracking error for a portfolio.

The first method is to simply make the difference between the portfolio return and the return from the index it is trying to replicate.

Tracking Error = Rp-Ri

- Rp= Return from the portfolio

- Ri= Return from the index

![]()

You are free to use this image on your website, templates, etc., Please provide us with an attribution linkArticle Link to be Hyperlinked

For eg:

Source: Tracking Error Formula (wallstreetmojo.com)

There is another method to calculate the tracking error of a portfolio with respect to the return from the index the portfolio is tracking.

The second method takes the standard deviation of the return of the portfolio and the benchmark.

The only difference is in this method; it is like calculating the standard deviation of return of the portfolio and that of the index the portfolio is trying to replicate. The second method is the more popular one and is used when the time series of data has a long history; in other words, when the historical data for the return of two variables are available for a longer period of time.

Table of contents

- Formula for Tracking Error (Definition)

- Explanation

- Examples

- Use of Tracking Error Formula

- Recommended Articles

Explanation

Tracking error is a measure to find out how much the return of a portfolio or a mutual fund deviates from the return of an index it is trying to replicate in terms of the components of an index and also in the term of the return of that index. But most of the time, it doesn’t get replicated exactly in terms of the return, due to various factors like the timing of buying the stocks, the personal judgment of the fund manager to alter the proportion depending on his style of investment.

Other than these, the volatilities of the stocks in the portfolio and the various charges that are attached for an investor when they invest in a mutual fund also result in deviation of the returns of a portfolio and the index the portfolio tracks.

Examples

You can download this Common Stock Formula Excel Template here – Common Stock Formula Excel Template

Example #1

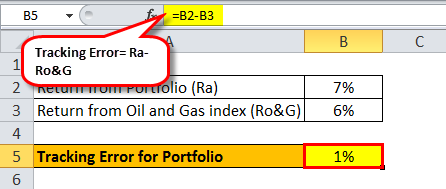

Let us try to do the calculation of the tracking error with the help of an arbitrary example, say for mutual fund A, which is tracking the oil and gas index. It is calculated by the difference in the return of the two variables.

Tracking Error calculation = Ra – Ro&G

- Ra= Return from the portfolio

- Ro&g= return from the oil and gas index

Suppose the return from the portfolio is 7%, and the return from the benchmark is 6%. The calculation will be as follows,

In this case, the tracking errors for the portfolio will be 1%.

Example #2

There is a mutual fund managed by a fund manager in SBI. The name of the fund in question is SBI- ETF Nifty Bank. This particular fund is constructed by taking the components of bank nifty closely in the proportion by which the banking stocks are in the bank nifty index.

Tracking Error = Rp-Ri

One year return from the portfolio is 8.9%, and the one-year return from the Nifty benchmark index is 8.6%.

In this case, the tracking errors for the portfolio will be 0.3%.

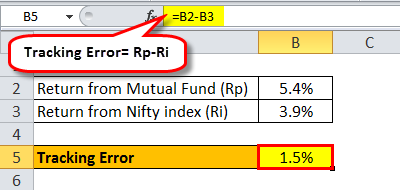

Example #3

There is a mutual fund managed by a fund manager in Axis Bank. The name of the fund in question is Axis Nifty ETF. This particular fund is constructed by taking the components of the nifty 50 closely in the proportion by which the index stocks are in the Nifty index.

One year return from the portfolio is 5.4%, and the one-year return from the Nifty benchmark index is 3.9%.

In this case, the tracking errors for the portfolio will be 1.5%.

Use of Tracking Error Formula

It helps the investors of a fund to understand whether the fund is closely tracking and replicating the components of the index it is putting up as a benchmark. It showcases whether the fund manager is trying to actively track the benchmark or he is putting his style in order to modify it. It also helps the investors to find out whether the charges are high enough for the fund to impact the return of the fund.

Recommended Articles

This has been a guide to Tracking Error Formula. Here we discuss how to calculate tracking error for the portfolio along with examples and a downloadable excel template. You can learn more about financing from the following articles-

- Calculate Sample Standard DeviationSample standard deviation refers to the statistical metric that is used to measure the extent by which a random variable diverges from the mean of the sample.read more

- Margin Error FormulaThe margin of error is a statistical expression to determine the percentage point the result arrived at will differ from the actual value. Standard deviation divided by the sample size, multiplying the resultant figure with the critical factor. Margin of Error = Z * ơ / √nread more

- Risk-Adjusted Return CalculationRisk-adjusted return is a strategy for measuring and analyzing investment returns in which financial, market, credit, and operational risks are evaluated and adjusted so that an individual may decide whether the investment is worthwhile given all of the risks to the capital invested.read more

- 529 Plan529 Plan or qualified tuition plan refers to a tax-advantaged savings plan whereby the parents or grandparents can save money for their children’s or grandchildren’s future education. Such savings are tax-free only when it is used for meeting the relevant educational costs.read more

From Wikipedia, the free encyclopedia

In finance, tracking error or active risk is a measure of the risk in an investment portfolio that is due to active management decisions made by the portfolio manager; it indicates how closely a portfolio follows the index to which it is benchmarked. The best measure is the standard deviation of the difference between the portfolio and index returns.

Many portfolios are managed to a benchmark, typically an index. Some portfolios are expected to replicate, before trading and other costs, the returns of an index exactly (e.g., an index fund), while others are expected to ‘actively manage’ the portfolio by deviating slightly from the index in order to generate active returns. Tracking error is a measure of the deviation from the benchmark; the aforementioned index fund would have a tracking error close to zero, while an actively managed portfolio would normally have a higher tracking error. Thus the tracking error does not include any risk (return) that is merely a function of the market’s movement. In addition to risk (return) from specific stock selection or industry and factor «betas», it can also include risk (return) from market timing decisions.

Dividing portfolio active return by portfolio tracking error gives the information ratio, which is a risk adjusted performance measure.

Definition[edit]

If tracking error is measured historically, it is called ‘realized’ or ‘ex post’ tracking error. If a model is used to predict tracking error, it is called ‘ex ante’ tracking error. Ex-post tracking error is more useful for reporting performance, whereas ex-ante tracking error is generally used by portfolio managers to control risk. Various types of ex-ante tracking error models exist, from simple equity models which use beta as a primary determinant to more complicated multi-factor fixed income models. In a factor model of a portfolio, the non-systematic risk (i.e., the standard deviation of the residuals) is called «tracking error» in the investment field. The latter way to compute the tracking error complements the formulas below but results can vary (sometimes by a factor of 2).

Formulas[edit]

The ex-post tracking error formula is the standard deviation of the active returns, given by:

![{displaystyle TE=omega ={sqrt {operatorname {Var} (r_{p}-r_{b})}}={sqrt {{E}[(r_{p}-r_{b})^{2}]-({E}[r_{p}-r_{b}])^{2}}}={sqrt {(w_{p}-w_{b})^{T}Sigma (w_{p}-w_{b})}}}](https://wikimedia.org/api/rest_v1/media/math/render/svg/fcbdc33801fc0d2e9791f95d3385b8096f049523)

where  is the active return, i.e., the difference between the portfolio return and the benchmark return.[1] The optimization problem of maximizing the return, subject to tracking error and linear constraints, may be solved using second-order cone programming:

is the active return, i.e., the difference between the portfolio return and the benchmark return.[1] The optimization problem of maximizing the return, subject to tracking error and linear constraints, may be solved using second-order cone programming:

Interpretation[edit]

Under the assumption of normality of returns, an active risk of x per cent would mean that approximately 2/3 of the portfolio’s active returns (one standard deviation from the mean) can be expected to fall between +x and -x per cent of the mean excess return and about 95% of the portfolio’s active returns (two standard deviations from the mean) can be expected to fall between +2x and -2x per cent of the mean excess return.

Examples[edit]

- Index funds are expected to have minimal tracking errors.

- Inverse exchange-traded funds are designed to perform as the inverse of an index or other benchmark, and thus reflect tracking errors relative to short positions in the underlying index or benchmark.

Index fund creation[edit]

Index funds are expected to minimize the tracking error with respect to the index they are attempting to replicate, and this problem may be solved using standard optimization techniques. To begin, define  to be:

to be:

where  is the benchmark return and

is the benchmark return and  is the covariance matrix of assets in an index. While creating an index fund could involve holding all

is the covariance matrix of assets in an index. While creating an index fund could involve holding all  investable assets in the index, it is sometimes better practice to only invest in a subset

investable assets in the index, it is sometimes better practice to only invest in a subset  of the assets. These considerations lead to the following mixed-integer quadratic programming (MIQP) problem:

of the assets. These considerations lead to the following mixed-integer quadratic programming (MIQP) problem:

where  is the logical condition of whether or not an asset is included in the index fund, and is defined as:

is the logical condition of whether or not an asset is included in the index fund, and is defined as:

References[edit]

- ^ Cornuejols, Gerard; Tütüncü, Reha (2007). Optimization Methods in Finance. Mathematics, Finance and Risk. Cambridge University Press. pp. 178–180. ISBN 978-0521861700.

External links[edit]

- Tracking Error — YouTube

- Tracking error: A hidden cost of passive investing

- Tracking error

- What is the Tracking Error?

A measure of the difference between the return fluctuations of an investment portfolio and the return fluctuations of a chosen benchmark

What is Tracking Error?

Tracking error is a measure of financial performance that determines the difference between the return fluctuations of an investment portfolio and the return fluctuations of a chosen benchmark. The return fluctuations are primarily measured by standard deviations.

Generally, a benchmark is a diversified market index that represents part of the total market. The most common benchmarks for equity portfolios are the S&P 500 and the Dow Jones Industrial Average (DJIA) for portfolios with large-cap stocks, and the Russell 2000 for small-cap portfolios.

Importance of Tracking Error

Tracking error is one of the most important measures used to assess the performance of a portfolio, as well as the ability of a portfolio manager to generate excessive returns and beat the market or the benchmark. Due to the abovementioned reasons, it is used as an input to calculate the information ratio.

Tracking error is frequently categorized by the way it is calculated. A realized (also known as “ex post”) tracking error is calculated using historical returns. A tracking error whose calculations are based on some forecasting model is called an “ex ante” tracking error.

Low errors indicate that the performance of the portfolio is close to the performance of the benchmark. Low errors are common with index funds and ETFs that replicate the composition of major stock market indices.

High errors reveal that the portfolio’s performance is significantly different from the performance of the benchmark. The high errors can indicate that the portfolio substantially beat the benchmark, or signal that the portfolio significantly underperforms the benchmark.

Formula for Tracking

Tracking efficiency is calculated using the following formula:

![]()

Where:

- Var – the variance

- rp – the return of a portfolio

- rb – the return of a benchmark

Example of Tracking Error

Five years ago, Sam invested $100,000 in Fund A. The fund primarily invests in large-cap US equities. During the five-year period, the fund showed positive returns. Also, the economy also grew during the period and equity markets rose.

In order to assess how successful his investment was, Sam decides to compare the returns of Fund A against the returns of a benchmark. In such a case, the most appropriate benchmark is the S&P 500 because it tracks the performance of the biggest large-cap companies.

The comparison of the fund against the benchmark can be measured using the tracking error.

The following data is available for the yearly returns for both Fund A and the S&P 500:

![]()

We can plug this data into the formula to calculate the tracking error:

![]()

In the scenario above, the small tracking error indicates that Fund A does not significantly outperform the benchmark. Therefore, Sam may consider withdrawing his money from the fund and putting it into other, more promising investment opportunities. Alternatively, he may be satisfied with the fact that his portfolio is keeping pace with the gains of the overall market.

Related Readings

Thank you for reading CFI’s guide on Tracking Error. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below:

- Exchange Traded Funds (ETFs)

- Index Funds

- Nasdaq Composite

- Small Cap Stock

- See all wealth management resources